tvOLS estimate time-varying coefficient of univariate

linear models using the kernel smoothing OLS.

tvOLS(x, ...) # S3 method for matrix tvOLS( x, y, z = NULL, ez = NULL, bw, est = c("lc", "ll"), tkernel = c("Triweight", "Epa", "Gaussian"), singular.ok = TRUE, ... ) # S3 method for tvlm tvOLS(x, ...) # S3 method for tvar tvOLS(x, ...) # S3 method for tvvar tvOLS(x, ...)

Arguments

| x | An object used to select a method. |

|---|---|

| ... | Other arguments passed to specific methods. |

| y | A vector with dependent variable. |

| z | A vector with the variable over which coefficients are smooth over. |

| ez | (optional) A scalar or vector with the smoothing values. If values are included then the vector z is used. |

| bw | A numeric vector. |

| est | The nonparametric estimation method, one of "lc" (default) for linear constant or "ll" for local linear. |

| tkernel | A character, either "Triweight" (default), "Epa" or "Gaussian" kernel function. |

| singular.ok | Logical. If FALSE, a singular model is an error. |

Value

tvOLS returns a list containing:

A vector of length obs, number of observations time observations.

A vector of length obs with the fitted values from the estimation.

A vector of length obs with the residuals from the estimation.

See also

Examples

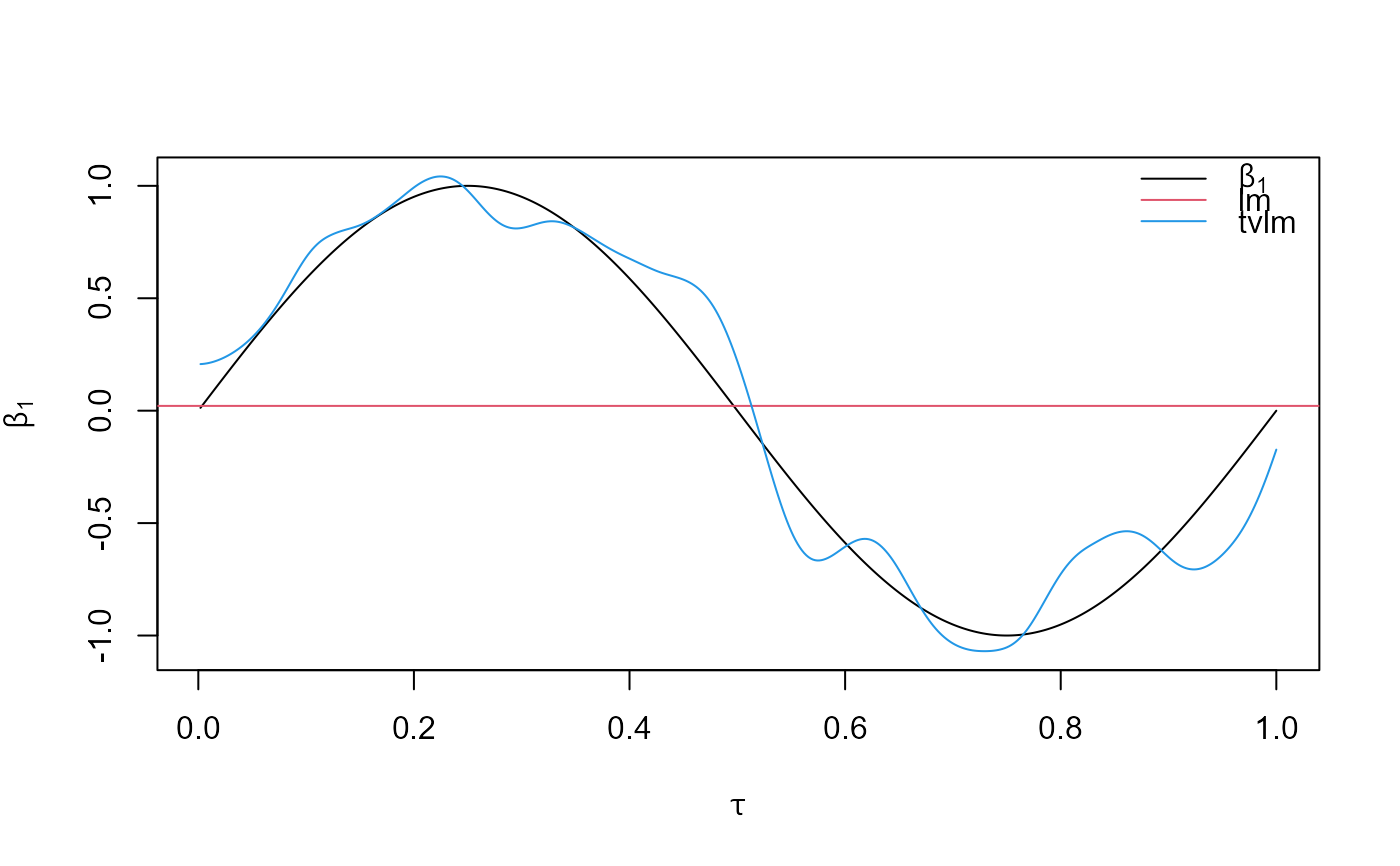

tau <- seq(1:500)/500 beta <- data.frame(beta1 = sin(2*pi*tau), beta2 = 2*tau) X <- data.frame(X1 = rnorm(500), X2 = rchisq(500, df = 4)) error <- rt(500, df = 10) y <- apply(X*beta, 1, sum) + error coef.lm <- stats::lm(y~0+X1+X2, data = X)$coef coef.tvlm <- tvOLS(x = as.matrix(X), y = y, bw = 0.1)$coefficients plot(tau, beta[, 1], type="l", main="", ylab = expression(beta[1]), xlab = expression(tau), ylim = range(beta[,1], coef.tvlm[, 1]))